Nowadays, Credit cards are an essential and reliable financial tool for many people, providing rewards and flexibility. High interest rates on outstanding balances can quickly turn this convenience into an economic liability. This is where 0 balance transfer credit cards come into the picture. These cards allow you to transfer current pending credit card debt to a newly issued credit card without interest rate for a specific period, helping you save money on interest and pay off your debt quicker.

In this guide, we'll explore everything there is to know about zero balance transfer credit cards without any interest, including how they work, their advantages, eligibility criteria, and detailed, step-by-step instructions on applying for one.

This write-up will focus on the basic idea of 0 balance transfer credit cards. These cards typically feature an interest-free introductory period of 6 to 18 months.

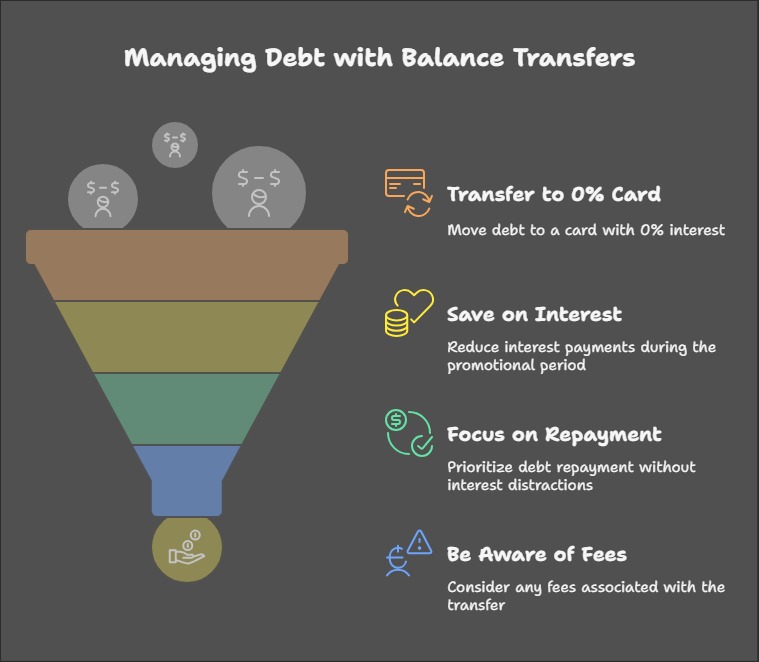

Credit card balance transfer processes allow you to move high-interest, existing debt to a different card with a lesser rate, helping you save money significantly.

Almost all credit card companies offer a certain service called Balance Transfer (BT).

This feature allows the cardholder to move their existing debt—the due amount on the card—to a different credit card account issued by a different financial organization or bank.

This arrangement is advantageous to both parties, as cardholders are given a chance to pay back their debts at a much cheaper interest rate. It also enables the banks to assist their clients in managing their debt.

Most banks attract cardholders with 0% interest balance transfer periods. With some banks, you can also pay back your debt with lesser interest by following an instalment plan or lowering the interest % for a set period.

When used effectively, a balance transfer can help you take charge of your debt, as these zero-balance credit cards often offer a 0% interest rate during the aforementioned introductory period of 6 to 18 months.

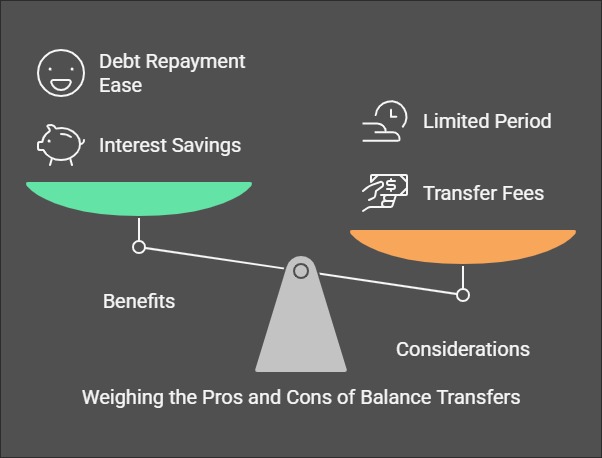

Now, not only are you saving a lot of money, but also paying off your debt more quickly. Keep in mind that these reduced interest rates apply only for a certain brief duration, post which regular interest rates will be in effect. Additionally, sometimes, an occasional fee may be associated with the amount being transferred, which will be added to your balance.

For those seeking a 0% interest balance transfer credit card in the UAE, several options cater to different income levels and fee structures.

ADCB (Abu Dhabi Commercial Bank) : This bank offers multiple choices. For instance:

365 Cashback Credit Card : This is one of the best options for people looking to get a zero-balance transfer credit card. It requires a minimum salary of AED 8,000. The ADCB 365 Cashback Credit Card has been recognised for its outstanding features, earning multiple awards for its innovative rewards program, convenience, and customer service. The card offers customers cashback on their everyday purchases, including groceries, dining, and fuel, providing them with a simple and convenient way to earn rewards while managing their finances. Additionally, the card offers a range of other benefits, such as complimentary travel insurance, access to exclusive discounts and offers, and much more.

365 Islamic Cashback Covered Card : To be eligible for the cashback rewards, you must make a minimum purchase of AED 5,000 or more within a calendar month. You can earn a maximum monthly cashback of AED 1,000 on your card

LULU Titanium Credit Card : Their LULU Titanium Credit Card, available with a lower salary requirement of AED 5,000, is free for life, while the LULU Platinum Credit Card demands AED 15,000 but also comes with a lifetime fee waiver. Experience the best of shopping and rewards with the Abu Dhabi Commercial Bank's ADCB LuLu Titanium Credit Card. In the UAE, cardholders can unlock a world of exclusive benefits and shopping conveniences. With the ADCB LuLu Titanium Credit Card, get ready for a premium shopping journey in the UAE that not only satisfies your lifestyle needs but also provides value with every transaction.

SHARE Signature Credit Card : FAB's lineup includes the SHARE Signature Credit Card, with a high AED 30,000 salary requirement and AED 1,500 annual fee.

SHARE Platinum Credit Card : SHARE Platinum Credit Card at AED 10,000 salary and AED 1,000 fee.

FAB Low-Rate Credit Card : The FAB Low-Rate Credit Card provides a more affordable option at AED 10,000 salary and AED 315 annual fee.

RAKBANK : This bank presents premium options such as the Emirates Skywards World Elite Mastercard, requiring an AED 20,000 salary with an AED 1,499 fee, and the World Mastercard Credit Card, which waives fees for the first year. The RAKBANK Titanium Mastercard (AED 8,000 salary) remains a strong contender for those looking for a lifetime free option. Every card is issued with benefits, making it important to choose based on both salary eligibility and long-term cost-effectiveness.

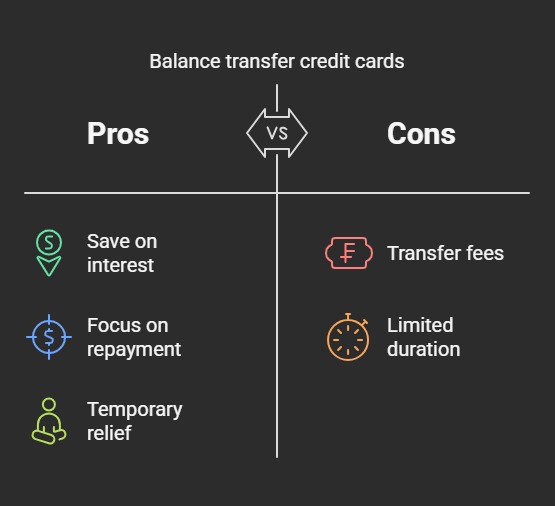

Listed below are the most important benefits of the 0 balance transfer credit cards :

Interest-Free Time Frame : Credit card companies offer a 12- to 18-month zero per cent interest period during the balance transfer process. In this time span, cardholders can settle the amounts on the credit cards, ensuring they don't incur any interest.

Readily Accessible : Most leading banks and financial organisations offer credit cards that come with an in-built balance transfer facility. It is easier than ever to connect with the specific credit card provider and get this service activated, to settle the bills.

Streamlining Debt : Debt streamlining is a method of consolidating credit card bills from multiple credit cards into a single credit card. Furthermore, streamlining debt in this way can help you more effectively handle the repayments of multiple credit card obligations by consolidating the debt. So, if you have more than two credit cards with balances, you can combine both and use a zero-balance transfer credit card with zero percent interest to pay one single bill.

Manage and positively impact a growing credit score : The process of using balance transfers assists clients in a more swift payoff of their debts, which reduces the amount owed and saves interest. People improve their credit scores by managing their money more effectively and responsibly.

Before applying for a 0% interest balance transfer credit card, keep in mind :

Ensure enough homework is done from plenty of market research, to get the best offer from the credit card company with multiple bonuses for debt transfers.

Balance transfers are only enabled once after your credit card is approved. So don't stop paying your debts on the other cards in a timely manner until the credit card is approved. Different banks have different processing time frames for approving balance transfers.

One of the most vital and significant aspects of your zero-interest balance transfer credit card is the interest rate. So, before applying for the card, make sure this is figured out. Almost all banks charge a small fee for all balance transfers.

There is no change to a person's credit limit upon using credit card balance transfers.

A cardholder cannot utilise the reduced interest rate for the credit card balance that was transferred to make new purchases with the credit card. The normal interest rates on the newly issued credit cards will apply to these transactions.

To be eligible for a 0-interest balance transfer credit card, the cardholder will have to have used the credit card from the same provider for at least a year. This is to prevent customers from repeatedly switching to multiple other credit card providers in order to leverage cheaper rates of interest.

One of the best ways to utilise the 0-interest balance transfer credit cards is to ensure you pay off all of your debts in the low-interest period or the free-interest rate term, as there is a significant reduction in the interest rate.

In case your credit card is still available post a previous credit card debt transfer, it is nevertheless suggested to wait before using it till all remaining transfer payments have been made and all future charges are paid in advance.

It is very important to thoroughly review and fully understand the terms and conditions, specifically the details outlined in the fine print, for every feature and benefit offered by the provider of the zero balance transfer credit card. This ensures you are fully aware of all requirements, fees, and restrictions.

Applying for a zero-interest balance transfer credit card is a simple process. Adhere to these steps to start :

Step 1 : Exploration and Comparing Cards. Opt for credit cards that offer 0 balance transfer elevations. Compare vital factors such as the tenure of the promotional period, balance transfer rates, and standard interest rates.

Step 2 : Check Your Credit Score. Review your credit report and, more importantly, the credit score to ensure you meet the card's eligibility criteria. However, consider perfecting it before applying if your score is low.

Step 3 : Gather the needed documents. Prepare similar documents as evidence of identity, evidence of income, and recent bank statements.

Step 4 : Submit Your Documents. Apply either online or in person by filling out the documentation form thoroughly and providing the necessary documents.

Step 5 : Wait for an approval. The issuer will duly review your documentation and shortly notify you of their decision. Approval times may vary but generally take many business days.

Step 6 : Transfer Your Balances. Once approved, follow the issuer's instructions to transfer your balances to the new credit card.

Pay More Than the Minimum Payment : While making the minimal payment each month keeps your account in good standing, it won't help you pay off your debt snappily. Aim to pay as much as you can to go above the minimum to reduce your top balance briskly. This will help you clear your debt before the promotional 0-interest period ends.

Maintain a Detailed Repayment Plan : Develop a clear and realistic repayment plan acclimatized to your fiscal situation. Calculate how important you need to pay each month to exclude the transferred balance before the promotional period expires. Use budgeting tools or apps to track your progress and stay on target.

Avoid Late Payments at All Costs : Late payments can't only affect hefty freights but may also beget the card issuer to drop the 0% interest offer. Set up automatic payments or reminders to ensure you don't miss a due date. Constantly paying on time also helps ameliorate your credit score.

Repel the Temptation to Use the Card for New Purchases : Numerous 0 balance transfer cards charge interest on new purchases incontinently, indeed, during the promotional period. To avoid accruing fresh debt, chorus from using the card for everyday charges or impulse buys. Focus only on paying off the transferred balance.

Examine Your Spending and Budget Closely : While working to pay off your debt, keep a close eye on your overall spending habits. Produce a yearly budget that prioritizes debt prepayment while still covering essential charges. Cutting back on unnecessary purchases can free up further funds to put toward your balance.

Be Apprehensive of Balance Transfer Freights : Most 0% interest balance transfer credit cards charge a figure, generally 3 to 5 of the transferred quantum. Factor this figure into your prepayment plan to avoid surprises. For illustration, if you transfer 5,000 with a 3,150 outstanding. Ensure the interest savings outweigh this cost.

Don't Close Your Old Credit Cards Incontinently : After transferring your balance, avoid closing your old credit cards right down. Doing so can negatively impact your credit application rate, which may lower your credit score. rather, keep the accounts open but chorus from using them to help further debt

Take Advantage of Financial Tools and Coffers : Numerous credit card issuers offer free fiscal operation tools, similar to spending trackers, payment calculators, and credit scores. monitoring. Use these coffers to stay systematised and motivated throughout your debt repayment trip.

Plan for the End of the Promotional Period : Mark the end date of the 0% interest period on your timetable and plan accordingly. However, consider transferring the remaining quantum to another 0 balance transfer card (if available) or explore other debt repayment options to avoid high-interest charges If you're unable to pay off the entire balance also.

Avoid Accumulating New Debt : The benefit of a 0 balance transfer credit card is to help you pay off existing debt, not to produce new fiscal scores. Commit to living within your means and avoid taking on fresh debt while you work toward getting debt-free.

Seek Professional Advice if Needed : If you're floundering to manage your debt or produce a prepayment plan, consider consulting a fiscal counsel or credit counsellor. They can give substantiated guidance and help you develop a strategy to achieve fiscal stability.

By following these enhanced tips, you can utilise the advantages of your balance transfer credit card, save lots on interest, and take a safe way toward fiscal freedom. Discipline and careful planning are crucial to making the utmost of this important fiscal tool.

0% interest balance transfer credit cards can be a useful tool for paying off existing debt if used responsibly. By figuring out how these cards work, their benefits, and potential liabilities, you can take full control of your fiscal future. Remember to deeply compare different cards, read the terms and conditions carefully, and maintain a sensible repayment plan to maximise the benefits of a 0% balance transfer credit card.

Yes, most issuers allow you to transfer balances from multiple different cards as long as the total amount doesn't exceed your credit limit.

The promotional duration typically ranges from 6 to 18 months, depending on the card and your creditworthiness.

Yes, most issuers charge an additional balance transfer fee, which is usually a small percentage of the transferred amount.

It's unlikely, as these cards are typically reserved for individuals with reasonable to good credit scores.

Any leftover balance will be subject to the bank's current interest rate, which can definitely increase your existing debt.

Recent Articles

Popular Articles

FABCashback Credit Card

Minimum Salary AED 5,000

Annual Fee AED 315

Rate 3.50%

We gather this information to assist you better and track your progress with the credit card application.

FABCashback Credit Card

Minimum Salary AED 5,000

Annual Fee AED 315

Rate 3.50%