A credit score is a numeric value that represents an individual's creditworthiness. It is an essential parameter that banks and other financial institutions consider to determine the risk of lending money to prospective borrowers. What is a good credit score in UAE? In the United Arab Emirates (UAE), a good credit score has increasingly become the standard for accessing loans, credit cards, and other financial products at favourable terms and conditions. Most residents ask themselves: What is a good credit score in UAE, and how to check my credit score in UAE? Additionally, knowing how to increase one's credit score effectively and efficiently in the UAE can go a long way in helping individuals sustain their financial stability and financial freedom and also help them gain access to better financial opportunities that may present themselves. This blog looks at these aspects in more detail, including the importance of maintaining a proper credit score, how to check it, and how to improve credit score in UAE . A good credit score can give residents access to a wide range of financial services, such as enjoying low interest rates and high borrowing capacity, thus making it an essential part of efficient and effective financial planning in the UAE.

The credit system used in the United Arab Emirates is strictly governed by an agency known as the Al Etihad Credit Bureau, otherwise referred to as the AECB. The agency collects, compiles, and maintains detailed credit data for individuals and businesses operating in the UAE. The AECB contributes significantly to the economy by giving each individual a credit score between 300 and 900. In this system, the greater the number, the more creditworthy, as this tells the lenders and other financial institutions that the individual is more likely to honour their financial obligations. A broad classification illustrated below illustrates the different credit score levels used in the UAE:

300 - 540 : Poor – High risk of default; most banks will decline loan applications.

541 - 650 : Fair – Moderate default risk; it may be hard to get a loan.

651 - 710 : Good – Low default risk; adequate for the majority of financial products.

711 to 745 : This is an excellent range, reflecting a very low probability of default on the debt; thus, lenders favoured it in the market.

746 - 900 : Excellent – Minimal risk, increased creditworthiness; access to the prime financial benefits.

A good credit score in UAE is usually 651 and above, with scores of 711 and above providing even more significant financial benefits. Lenders prefer higher scores since they indicate good borrowers, resulting in quicker approvals, lower interest rates, and improved credit limits. A favourable credit rating is a prime consideration that not only determines the chance of obtaining loans and credit cards but also influences other aspects of one's finances in the United Arab Emirates. For example:

Lower Interest Rates : People with a good credit score tend to get lower interest rates on various financial products such as loans and credit cards. To illustrate, a consumer who has achieved an excellent credit score of 750 may be able to obtain a personal loan with a reasonable interest rate of 4%. In contrast, a consumer whose credit score is significantly lower, i.e., around 600, may have to pay substantially higher interest rates, perhaps even 7% or even more, for the same type of loan.

Increased Credit Limits : People with good credit scores can obtain more extensive credit limits. Accessing such significant credit limits can be extremely useful during financial emergencies when surprise bills occur, and more money is needed.

More straightforward Loan Approvals : Banks and other financial institutions are more likely to sanction loans of any kind, like mortgage loans, car loans, or personal loans, for those with a good credit history. For example, take the case of an individual who has attained a credit score 720; this person is bound to have a smooth approval process while applying for a home loan of AED 500,000. However, a person with an inferior credit score 580 will likely face severe hardship while trying to qualify for any loan.

Better Rental Agreements : When leasing houses, landlords typically consider potential renters' credit records to assess whether they are financially stable and reliable. A better credit rating can even lower the security deposit paid, or in some instances, it can even eliminate the necessity of making a big initial payment.

Impact on Career : Some employers, particularly those in the banking and finance industries, typically go the extra mile of checking credit scores as part of their hiring process. Good credit reflects good financial planning and can go a long way in enhancing one's professional prospects in these extremely competitive industries.

Given the many benefits of having a good credit rating, taking proactive steps to ensure a good credit rating is imperative. This can be done by diligently practising good money habits, such as making timely payments of instalments on whatever debts one owes, handling debt thoughtfully and prudently, and occasionally checking one's credit report to ensure everything input into it is correct and current.

It is essential to know your credit score to efficiently maintain and sustain your overall financial well-being in the United Arab Emirates. The following is a compilation of ways you can obtain and view your credit score:

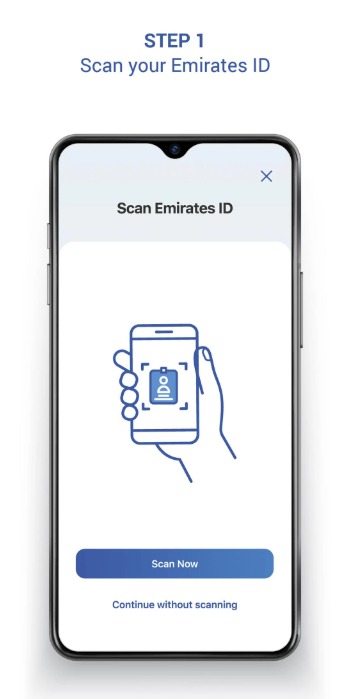

Method 1 : You can easily access Al Etihad Credit Bureau (AECB) services either from the official Website or the Mobile Application they have launched.

Step 1 : Log in to the Platform

https://play.google.com/store/apps/details?id=com.aecb.app&hl=en_IN&pli=1

Website : Go to the official AECB website at aecb.gov.ae.

Mobile App : You can download the app titled "AECB Credit Credit Report is readily available on both the App Store and the Google Play Store.

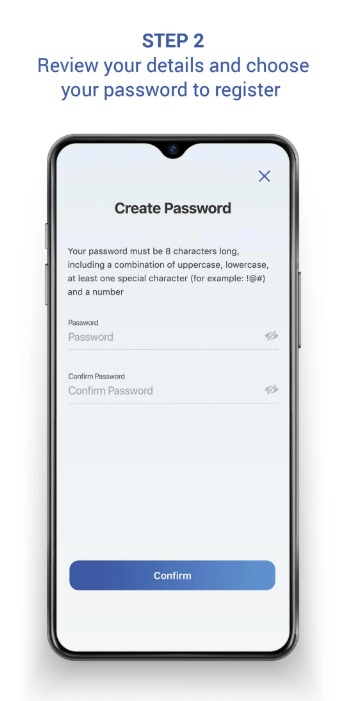

Step 2 : Either register yourself or log in to your account if already registered.

https://play.google.com/store/apps/details?id=com.aecb.app&hl=en_IN&pli=1

New Users : Sign up by scanning your Emirates ID and entering your personal information.

Existing Users : Login with your already created credentials.

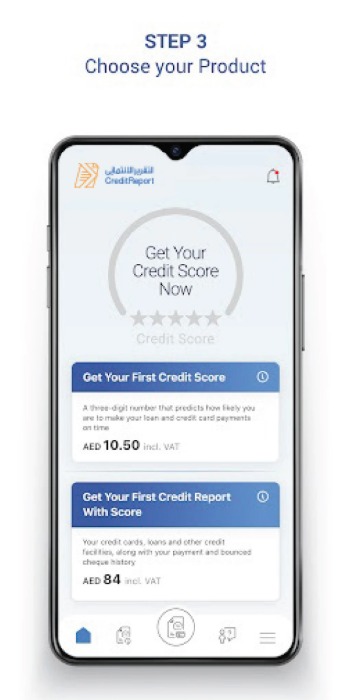

Step 3 : Choose the Target Report

https://play.google.com/store/apps/details?id=com.aecb.app&hl=en_IN&pli=1

Credit Score : A three-digit rating given to you to express your creditworthiness.

Credit Report : A detailed document listing your credit history, such as your credit score, payment record, and other financial obligations.

Step 4 : Move on to Finish the Payment Process

https://play.google.com/store/apps/details?id=com.aecb.app&hl=en_IN&pli=1

Credit Score : AED 10.50 (including VAT).

Credit Report : AED 84 (VAT inclusive).

They can be paid safely using a debit card or a credit card.

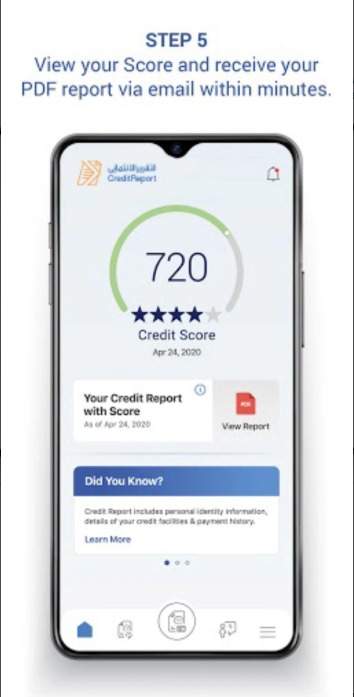

Step 5 : Look at Your Data

https://play.google.com/store/apps/details?id=com.aecb.app&hl=en_IN&pli=1

After your payment has been processed successfully, your report or credit score will be ready for you to pursue. A copy will also be sent to the registered email address.

Method 2 : Through UAE Banks and Financial Institutions

Several UAE banks partner with AECB to provide their customers with access to their credit reports:

Emirates NBD: Clients can now apply for their credit score online, courtesy of the bank's partnership with AECB.

Abu Dhabi Commercial Bank, or ADCB, offers services designed explicitly for credit scores and reports.

First, Abu Dhabi Bank, also popularly known as FAB, provides informative and detailed information relevant to its customers' credit scores.

Method 3 : In person at the AECB Customer Service Centers, where customers can personally deal with representatives.

For individuals with high face-to-face interaction preference:

AECB Centers : Situated all over the UAE.

Documents Required : You must provide the original Emirates ID and a photocopy of your passport.

Payment : Fees can be paid quickly through one of the alternatives, e.g., credit cards, debit cards, or eDirham cards.

Method 4 : Through the TAMM Platform

Abu Dhabi residents can easily view their individual credit information using the easily accessible TAMM platform, which has been designed to make this service effective.

To view, please log in via the UAE Pass function on the TAMM application.

Navigation : To see your information, please choose the "Credit Report and Credit Score."

Getting a better credit score in the UAE takes planning and following through. These are some good ways to help you improve your creditworthiness:

1. Paying your bills on time : How well you pay your bills dramatically affects your credit score. Paying all your bills on time, including rent, credit cards, loans, and utilities, shows that you are responsible with money and can help your credit score.

2. Manage your credit use : Keep your credit card amounts low compared to your credit limits. A high ratio of credit usage can hurt your score. Try to use no more than 30% of the credit you have access to to show lenders you can responsibly handle credit.

3. Limit New Credit Applications: Every time you ask for new credit, your credit report gets a hard inquiry, which can bring down your score a little. Using this effect more than once in a short amount of time can make it stronger. You should only apply for new credit when you need it.

Yes, expatriates holding an Emirates ID can even access credit scores with ease with the help of the services of the AECB as well as through the services of partner banks that facilitate this.

Your credit score is affected by how long you've had credit. Keeping old accounts open, even if you don't use them often, can show that you've been good with money for a long time. But make sure these accounts are handled correctly.

5. Diversify Your Credit Mix : Different types of credit, like mortgages, credit cards, and personal loans, can help your credit score because it shows that you can adequately handle different types of credit.

6. Review Your Credit Report Regularly : Getting and reading your credit report regularly can help you find and dispute any errors that may be lowering your score. You can get your credit record from the UAE's Al Etihad Credit Bureau (AECB).

7. Pay off your debts : Paying off your debts should be your priority. Pay off the bills with the highest interest rates first. If you are having trouble with money, you should talk to your creditors about payment plans.

8. Think About Credit-Builder Products : Some banks offer products that help people build or fix their credit. These include secured credit cards and credit-builder loans, which, if used properly, can help you create a good payment history.

To raise your credit score slowly, you need to be steady and responsible with your money. These tips can help you improve your credit score and have better financial chances in the UAE.

A good credit score is a significant financial asset in the United Arab Emirates, as it has a massive impact on a range of important areas, such as loan approvals, interest rates, rental contracts, and employment opportunities for those seeking employment. To ensure that one has a good credit score, good and correct financial habits are needed, which involve paying bills on a regular and timely basis, actively paying off dues on loans and other borrowings, and regularly checking credit reports for accuracy and any discrepancies that may occur. By checking their credit scores now and then through the Abu Dhabi Economic Department's AECB or partner agencies, individuals can make proactive and informed choices to improve their overall financial health and well-being. Understanding what a good credit score in the UAE is, how one can check their credit score in the UAE, and the different ways in which one can enhance their credit score in the UAE provides residents with the knowledge they need to make more timely and informed financial choices, thus allowing them to attain more economic opportunities and rewards in the future.

It is strongly recommended that you review your credit score at least every three to six months to ensure accuracy and be in a place to monitor any progress that could have been made over time.

Although building a credit score typically takes a long time, several methods can be employed. Through paying off debts, maintaining timely payments, and reducing the credit utilization ratio, one can perhaps obtain a significant improvement in their credit score within a few months.

The answer is no; requesting your credit score from organizations like AECB or any other bank does not impact your credit score. But I must mention here that if there are several hard inquiries by lenders, those can decrease your credit score in the long run.

A poor credit score can lead to loan refusals, increased interest rates, and trouble obtaining financial products. Better financial behaviour can improve the score over time.

Yes, expatriates holding an Emirates ID can even access credit scores with ease with the help of the services of the AECB as well as through the services of partner banks that facilitate this.

Recent Articles

Popular Articles

FABCashback Credit Card

Minimum Salary AED 5,000

Annual Fee AED 315

Rate 3.50%

We gather this information to assist you better and track your progress with the credit card application.

FABCashback Credit Card

Minimum Salary AED 5,000

Annual Fee AED 315

Rate 3.50%